Fixed rate mortgages are low once again. Now is a good time to buy. But what if you already own a home. Could refinancing be right for you? Could an adjustable rate loan be right? Here are some factors that would influence your decision. How long are you going to stay in your home? Which option gives you the cheapest cost for housing?

Fixed rate mortgages are low once again. Now is a good time to buy. But what if you already own a home. Could refinancing be right for you? Could an adjustable rate loan be right? Here are some factors that would influence your decision. How long are you going to stay in your home? Which option gives you the cheapest cost for housing?

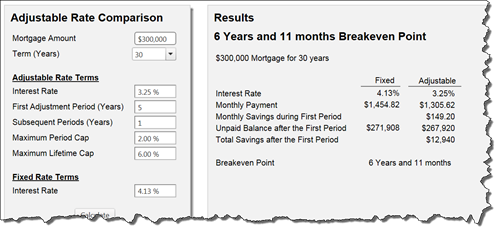

As an example, if we compare getting a $300,000, 30-year term fixed mortgage at 4.125 percent or 3.25 percent on a 5/1 adjustable, your breakeven point would be at the seven year mark if, worst case, the rates adjusted their set maximum amount each year.

Using that information, if you are planning on staying in your home less than 7 years, this specific Adjustable Rate Mortgage or ARM would give you a cheaper cost of housing. My example above shows that by the end of five years, your ARM would generate about $13,000 in savings over a fixed-rate mortgage.

Now if you are a homeowner with an existing ARM, you might want to reconsider financing into a fixed-rate mortgage. If you find that you will be staying longer in the home than previously thought, convert to a fixed-rate to lock in your payment from month to month and get your monthly housing costs set. There are few surprises with a fixed-rate mortgage.

I suggest you consult a mortgage professional to get a full explanation of fixed-rate and ARM products available and at what interest rates. Plug your own numbers into my example above and see what your outcome would be.